I recently listened with interest to the comments aired on the news program 60 Minutes by Dr. Martin Cooper, the inventor of the cell phone (Browning, 2010). As Dr. Cooper put it, when product engineering is driven predominantly by a fascination with technology, or by the desire to impress competitive engineers rather than by the needs of its customers, it can move off the path of what the customers of that technology actually want. As an example, he pointed to the fact that the user manuals that come with today's cell phones are not only bigger than the cell phone itself, but are complex tomes describing numerous capabilities customers never asked for and may never use.

Similarly, when corporate business decisions in any industry are driven predominantly by the desire to, for example, become the world's largest in that industry, or in an effort to marginalize a competitor, these corporations can move off the path of what is in the best interests of their customers.

For the last decade, my colleagues and I have both recognized and have tried to share with the audiology community several key factors vital to the audiology profession's future growth and success:

- All forms of audiology practice are essential for the audiology profession's survival, but independent, autonomous practice is particularly critical:

- As corporate businesses continue to acquire and manage larger segments of the United States hearing care provider market, fewer independent and autonomous practice opportunities will be available and/or survive.

- Using millions of marketing dollars, business corporations continue to define hearing care to the American consumer as predominantly a commodity-based purchase transaction (i.e., hearing aids).

- Collectively, audiology is an enormous "customer" to most of these corporate businesses, and as such, has the potential to influence the decisions these businesses make.

- There is an ever-narrowing window of opportunity for audiology to capitalize on this influence. Once control of the buying decision is lost, so is the economic influence it represents.

a. Independent practices answer to no one other than their patients and with nothing other than their professional abilities when determining the services they provide, what they charge for those services, and what products (if any) are the best to treat those patients.

b. Independent practice ownership offers the greatest income potential, and is nearly double that of wage-based audiology compensation - a factor that is critical in response to the significantly greater cost and time now associated with earning the advanced degree. In addition, private-practice incomes positively affect the salary opportunities for wage-based positions.i. A large component of this income advantage remains tied to hearing aid dispensing.c. Independent practices can market themselves any way they want - including marketing the value and importance of evidenced-based audiology care available as a result of their education and training.

This updated report attempts to summarize the 2011 status of U.S. hearing-care-provider corporatization, and documents the changes that have occurred since 2004. This report once again puts these changes into the context of the audiology profession, and identifies the role both business corporations and audiology professionals play in shaping the profession's future.

Update on Corporate Ownership of U.S. Hearing Care Distribution

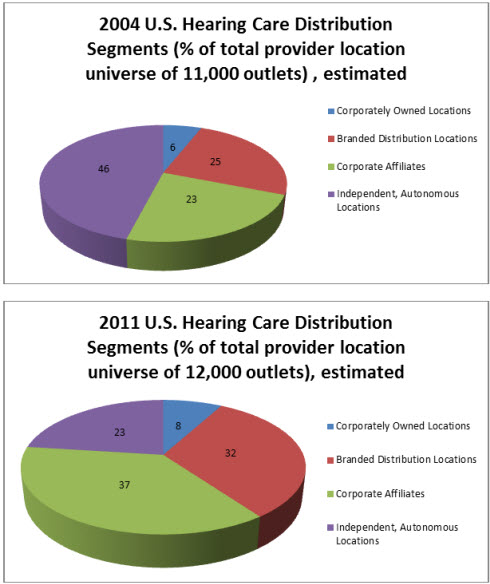

Figure 1 compares the corporate ownership information provided in the 2004 report referenced above with current 2011 information as reported by the same or similar public records used to compile the 2004 data, along with estimated data as detailed later in this paper. As stated in the 2004 report, the categories of distribution listed in this figure are as follows:

Company-owned Outlets: Provider outlets that have been purchased by and are fully owned by the consolidating corporation. In company-owned outlets the staff, both professional and administrative, are employees of the corporation. The overhead expenses of the practice are the responsibility of the corporation.

Branded Distribution Outlets: Provider outlets that are uniquely branded as a chain and are nationally promoted directly to the consumer by the business corporation that owns the retail brand. Participants sign agreements to exclusively distribute and represent the retail brand being promoted. The manufacturer or corporation who owns the retail brand spends the money needed to promote the brand nationally and forwards the leads acquired by this promotion to the chain's participants. Practice overhead remains the responsibility of the practice owner.

Affiliated Providers: Provider outlets that contract to buy products from or through a business corporation. In this case, an otherwise independent practice agrees to purchase some or most of their hearing aids from or through a business corporation that may also own provider outlets and/or branded distribution chains. The corporation can set the price these independent practices pay for their hearing aids - a price that also includes a profit margin that the corporation can invest any way they wish. They may also set prices for the services that the provider provides under the agreement. Practice overhead remains the responsibility of the practice's owner. Professional and support staff are not employees of the corporation. In some cases, these agreements may include providing the corporation with "first right of refusal" to buy the independent practice once it is up for sale.

Figure 1. Comparison of estimates of U.S. hearing care distribution segments between Fall 2004 and June 2011.

Based on these figures, it is estimated that the percentage of provider locations in the United States that are independently owned, autonomous in their decision-making and unaffiliated with a corporate business owner have gone from 46% of the 11,000 locations in 2004 to 23% of 12,000 outlets in 2011.

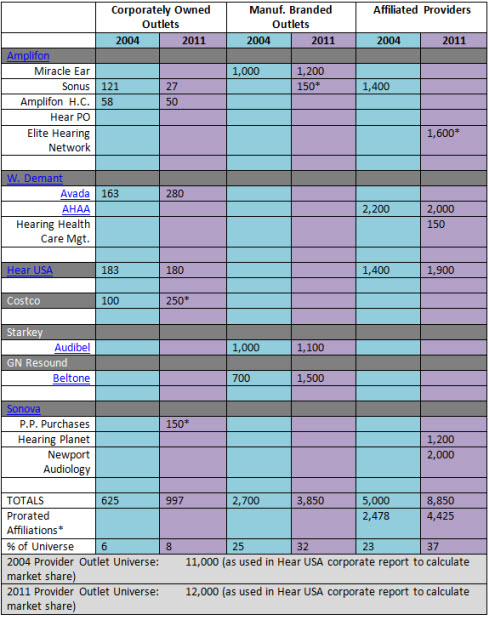

The raw data behind the estimates in these figures is provided in Figure 2. Most of these data are directly available from the companies' Web sites and other public documents listed in Appendix A. However, there are a few estimated data in Figure 2 that are designated with an asterisk.

Figure 2. Raw data behind comparison of U.S. hearing care distribution segments between Fall 2004 and June 2011. Estimated data is designated with an asterisk. Click Here to View a Larger Version of Figure 2 (PDF)

The estimated data in Figure 2 were based on the following:

- Sonus: Since the 2004 report, Sonus has been converting their corporately owned stores into the Sonus Franchise operation. Based on personal communications and observation, we estimate that there are approximately 30-35 Sonus franchisees that operate approximately 150 outlets in the United States under the Sonus brand.

- Amplifon: Amplifon lists 1,600 outlets under HearPO, and lists 1,600 outlets under the Sonus Elite program, which lists as one of its membership features receiving HearPO leads. We are assuming that these are the same 1,600 outlets, and therefore have listed them once under the Sonus Elite program.

- Costco: The Costco figure for 2011 is an estimate of U.S. outlets based on Costco's reported figures of nearly 300 outlets in the U.S., Canada, Mexico and Puerto Rico.

- Sonova: Several private-practice purchases by Sonova over the last five years have been identified through personal communications with parties involved. Based on this information, the national purchase figure of 150 listed here has been estimated, but is not confirmed.

- Prorated affiliation: Prorating the affiliated provider total is done to account for the likelihood that individual practice locations participate in more than one affiliated provider program. In 2004, the participation total number was approximately divided by 2 to prorate the locations involved, which revealed a figure of 23% of the total outlet universe. In 2011, the raw participation figure increased by 44%, and dividing by 2, revealed a figure of 37% of the total universe.

Amplifon, a public company headquartered in Milan, Italy, describes itself as a "world leader in hearing aid distribution" (Amplifon, 2011). Amplifon owns 100% of Miracle Ear, Sonus and National Hearing Centers- outlets located in Walmart stores which have since been re-branded as Amplifon Hearing Centers. As part of the Sonus acquisition, Amplifon also acquired HearPO, a company that manages third-party payer contracts nationally. HearPO leads are forwarded to participants in the Elite Hearing Network program, which numbers 1,600 locations. Established after 2004, the Elite Hearing Care Network provides marketing and management support to its members, as well as HearPO leads. In addition, since 2004 a number of the Sonus corporately-owned locations have been transitioning into the Sonus Franchise system. Franchised stores are locally owned, carry the Sonus brand, and maintain a corporately defined store design. In addition, franchisees pay a fee to underwrite the corporation's brand marketing activities to consumers. In addition, future store ownership transitions may be subject to corporate approval.

William-Demant is a public company headquartered in Copenhagen, Denmark. The company invests in manufacturing and distribution of hearing aid and communication products globally. In 2004, William-Demant owned hearing aid manufacturers Oticon and Bernafon. Since then, they have acquired Sonic Innovations. In addition, William-Demant owns a variety of audiometric equipment brands including Amplivox, Grason-Stadler, Interacoustics and Maico Diagnostics. They also own Phonic Ear and Sennheiser personal communications devices. By 2004, William-Demant had minority ownership of AHAA and Avada, two retail distribution companies in the U.S. In addition, since 2004 William-Demant has expanded their influence on hearing care distribution in the U.S. through acquisitions of the Hearing Care Management group purchasing organization (with outlets in 15 states) and equipment supply companies such as HIMSA (NOAH software), Gordon-Stowe and Associates (a large mid-west special instrument distributor) and most recently Northeastern Technologies Group and Mid-lantic Technologies Group (both special instrument distributors in the east).

HearUSA is a public corporation that was traded on the New York Stock Exchange until its bankruptcy filing in May of 2011. Since its inception in 1986, Hear USA has grown to a network of wholly owned and affiliated distribution centers across the United States. The corporation secures managed care contracts that are then serviced through this network of outlets. In 2010, HearUSA signed an agreement with American Association of Retired Persons (AARP) to establish the AARP Hearing Care Program - a program offering an AARP-endorsed member benefit for hearing testing and hearing aid purchase. This has resulted in their expansion of affiliated providers to 1,900, with the expectation that the affiliated provider base will be 5,000 by the end of 2011. HearUSA has had a long-standing relationship with Siemens, including ownership of HearUSA shares and loans to HearUSA in exchange for hearing aid purchasing commitments. Recently, a dispute regarding the disbursement of profits generated through the sale of a Canadian distribution asset by HearUSA has prompted both court action and the bankruptcy filing by the company. OnAugust 1, 2011, HearUSA announced an agreement for the sale of its assets toSiemens.

Costco is a public corporation traded on the New York Stock Exchange, is currently the third largest retailer in the U.S., and ranks at number 28 on the Fortune 500 list money.cnn.com/magazines/fortune/. Costco operates nearly 300 hearing aid centers in stores within the U.S., Canada, Mexico and Puerto Rico.

GN ReSound is one of several companies owned by Great Nordic, a public corporation headquartered in Copenhagen, Denmark. The ReSound Group includes hearing aid manufacturers ReSound and Interton, audiometric equipment manufacturer Otometrics, and U.S. retail hearing aid distributor Beltone. Beltone was acquired in 2000 and has more than doubled its outlet count in the U.S. since 2004.

Starkey Laboratories is a privately held hearing aid manufacturing company in Minnesota. In the 2004 report, the hearing aid distribution chain Audibel was reported to be affiliated with Starkey, who manufactures the Audibel product line, and listed William Austin as its CEO. In 2011, Audibel claims 1,100 provider locations and actively promotes and indicates participation with the Starkey Foundation.

Sonova is a publicly held corporation headquartered in Switzerland. Sonova was not included in the 2004 report, but has since made their presence known through acquisitions of hearing instrument manufacturers Phonak, Unitron and InSound Medical (Lyric). Additional manufacturing acquisitions include Sona, Phonak Communications, Advanced Bionics and Acoustic Implants. On the distribution side, Sonova has made distribution investments in Europe and China and count among their distribution purchases in the U.S. Hansaton, Hearing Planet, and Newport Audiology. An undisclosed number of audiology private practices in the U.S. have also been purchased by Sonova.

Audiology's Future

What makes the corporatization of hearing care distribution in the United States so important is the impact it could have on the availability and viability of independent practice ownership for audiologists and the impact it could have on patient care decision-making. Although the percentage of working audiologists who own a private practice is only 14%, their income is nearly twice the national average of salaried audiology positions (American Academy of Audiology, 2009). With the time and money now required to earn an audiology degree, this income option not only needs to be preserved, it needs to grow.

In order for audiology to own the profession now and in the future, it seems reasonable that audiology must first autonomously own the delivery of audiology care, which includes both the diagnosis and treatment of hearing and balance disorders. If the majority of audiologists are either employees of, or affiliated with, a business in which the value and importance of audiology care is marginalized either 1) in deference to medical care, 2) in deference to product delivery goals (hearing aid sales), or 3) by presenting the providers as "hearing care professionals", whether these providers hold an audiology degree or not, then owning the profession and/or owning the services it provides cannot occur. If the substantive value and importance of audiology care is not directly and specifically marketed by the employing business or the affiliated business entity so that audiology care is visible, recognized and demanded by the general patient population, it will be very difficult for audiology to be recognized as the entry point for hearing and balance care by either the general population, Medicare, insurance companies, or the medical profession.

When audiologists do not control the business's mission or its marketing dollars, they do not control the business's message to the public. The corporations that are buying up hearing care distribution are typically not in the business of marketing audiology care to consumers or exclusively using audiologists as their providers. They are in the business of selling hearing aids. So, as the autonomous share of the U.S. hearing-care delivery pie gets smaller, the likelihood that audiology will own its profession or be recognized as the entry-point for hearing and balance care decreases.

The audiology community must recognize that as much as audiology is a science and a health care profession, audiology is a business, and must be run like a business just like medicine, dentistry and optometry. Without both knowledge of and control of the "business" side of the audiology profession, it will be difficult to control audiology's destiny. And, this business acumen must extend beyond that needed to run and market an audiology private practice. Audiologists, whether in an autonomous practice or not, must also promote the profession nationally as the essential provider of hearing and balance health care. Effectively promoting audiology in this fashion is, by necessity, a commercial enterprise requiring a large-scale economic resource. Such a resource can be established in perpetuity if audiologists choose to leverage their commercial buying power collectively. This is necessary because the hearing care industry's manufacturers, corporations and non-audiology employers will not be promoting the audiology message with the marketing dollars they invest.

As a business tool, group purchasing shifts a great deal of an industry's business and financial control back into the hands of the customer. Further, a group purchasing organization that is structured to enroll only audiologists, and to direct the financial resources it receives toward marketing audiology care nationally, can uniquely build strong consumer recognition and demand for audiology care instead of products. Once this demand is established, the audiology profession will be capable of both owning the profession and being recognized (by the public and others) as the entry-point for hearing and balance disorders. This not only benefits the audiology profession, but benefits the industry and public sectors, as it creates a more powerful and lasting consumer connection than product.

In the May-Jun 2011 issue of Audiology Today magazine, Barry Freeman and James Steiger explored whether or not the audiology profession is making progress in becoming an autonomous profession since the inception of the Au.D. degree requirement. When four-year Au.D. programs were just getting started, Doyle and Freeman (2002) surveyed and compared the responses of four-year entry-level Au.D. students with master's students. At that time, 61 percent of Au.D. students expressed interest in owning their own private practice, compared with only 21 percent of master's students. In addition, 73 percent of Au.D. students indicated that, as audiologists, they would be the primary income earner in their family compared with only 50 percent of master's audiologists. In 2010, Bennet and Steiger re-surveyed audiology students and showed that only 24 percent of current Au.D. students prefer to own a practice. When asked if audiology is an autonomous profession, only 11 percent of current Au.D. students answered affirmatively; 44 percent of current Au.D. students have doubts about their career choice.

Based on this data, moving audiology to a doctoring profession is not proving to be the answer in securing audiology's autonomous future. It does not take a crystal ball to foresee that if audiology continues on its current course, the profession envisioned by the torch bearers of the Au.D. movement will not be realized. However, securing nationwide consumer recognition and "demand" for audiology care can certainly be a powerful foundation upon which audiology's future can be nurtured, and is arguably a necessary environment in order for audiology's autonomy to be established. This can only happen if audiology 1) commits to competing at the commercial level for the minds and hearts of America's hearing and balance patients, and 2) delivering a patient care experience that is second to none. Audiology-focused group purchasing (like AuDNet, Inc.) that uses group-purchasing revenue to nationally market and promote audiology care, and that can underwrite audiology-favorable political and legislative action, can accomplish the first. Each individual audiology practitioner must take responsibility to accomplish the second.

So, let's make securing nationwide consumer recognition and demand for audiology care a goal of the profession. Let's recognize that, in contrast to the various philanthropic attempts that have failed to reach this goal in the past, the audiology community must now commit as a group to leveraging its collective economic strength and market audiology care competitively on a nationwide basis to secure meaningful consumer recognition and demand for audiology care. If we do this, we can indeed build a strong future for the audiology profession rather than leaving that future to the decision-making of business forces outside of the profession. It is time audiology leveraged, for its own benefit, the buying power audiology represents and the expertise audiology embodies.

APPENDIX A

Data in Figure 2 was taken from the following sources, except where indicated.

AHAA, www.hearingreview.com/insider/2007-01-04_03.asp

Amplifon, www.amplifonusa.com/

Amplifon Q1-2001 Financial Results, page 11: www.amplifon.com/wps/wcm/connect/

Avada, www.avada.com/about-us.shtml

Beltone, www.beltone.com/

HearUSA, www.hearusa.com/BottomMenu/InvestorRelations.aspx

Why Audibel, from: www.demant.com/releasedetail.cfm?ReleaseID=577828

William Demant Holdings A/S, www.demant.com/about.cfm

Sonova, www.sonova.com/en/about/Brands/Pages/default.aspx

REFERENCES

American Academy of Audiology. (2009). Compensation and Benefits Report. Bainbridge Island, WA: Precision Reports, LLC.

Amplifon. (2011). World leader in personal hearing solutions. Retrieved August 2, 2011, from www.amplifonusa.com

Bennet, H., & Steiger, J. (2010). AuD student attitudes toward the profession: A 2002 survey repeated in 2009. Audiology Today, 22(6), 53-63.

Browning, D. (Producer). (2010, May 21). 60 Minutes [Television program]. New York, NY: CBS News.

Doyle, L.W., & Freeman, B.A. (2002). Professionalism and the audiology student: Characteristics of master's versus doctoral degree students. Journal of the American Academy of Audiology, 13(3), 121-131.

Freeman, B., & Steiger, J. (2011). The professionalization of audiology: Are we making progress? Audiology Today, 24(3), 43-45.

Smriga, D. (2004). Are we asleep at the wheel? The delicate future of audiology private practice in America. Feedback (the official publication of the Academy of Doctors of Audiology), 15(4), 7-15.